DIY InvestorMagazine

/

March2014

DIY InvestorMagazine

/

March2014

12

13

ALONGTERMPLAN

FORYOUR ISA

With over 30 years experience in Financial Services David (DAN) Norman has worked for 10

different firms, most recently the CEO of Credit Suisse Asset Management (UK) he founded

the specialist multi-asset passive boutique, TCF Investment, in 2009. Here he gives his

thoughts on the best long term strategy for your ISA.

STARTWITHTHEEND INMIND

Investing is like any other long term activity – it needs

a clear destination or purpose (tomake sure you can

monitor your progress), you need to understand the

risks that might be faced along the way (and what you

might need to do to reduce or to respond to those risks)

and it needs some determination to stay the distance.

A clear plan of what resources you will needed for later

life is critical – as the famous conversation in Lewis

Carroll’s ‘Alice’s Adventures InWonderland’ highlights:

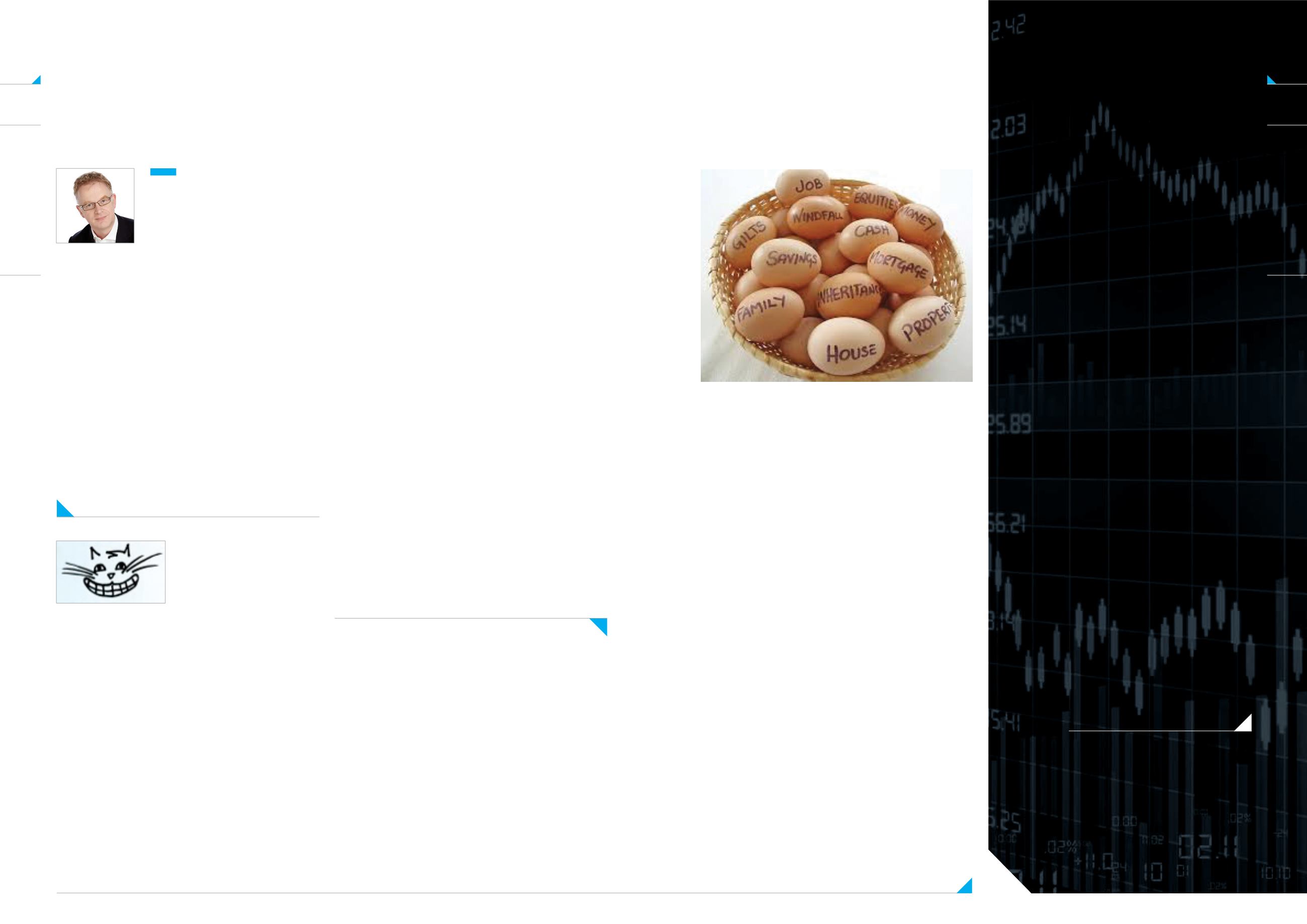

Diversification, the idea that spreading your investment

between different asset classes and between different

stocks within each asset class, can boost your returns

has been around for many years, but is as valid today as

it ever was.

Often described as a ‘free lunch’, you can boost your

returns and reduce your risk by diversifying and re

balancing regularly (bringing your portfolio back into

line with its long term asset allocation).

As a rule of thumb, more often than annually and less

often than quarterly is a good guide – the costs of re

balancing being a key factor. Spreading your investment

between assets classes (equities, bonds, property, cash,

commodities) leads to a lower risk profile.

The same goes for spreading investments within asset

classes between different geographies (e.g. UK and

Overseas) and sectors (e.g. energy, financial and retail

company shares). Index funds are an excellent way to

achieve this diversification at very low cost – they hold

a very broadmix of bonds or shares.

And rebalance very efficiently. The latest generation of

low cost multi - asset funds also offer diversification

across asset classes and can be very cost effective.

THERISKS

There are some obvious and less obvious risks that all

investors face. Chief among them are inflation, volatility

(the ups and downs) and cost – though I would argue

that costs aremore of a certainty than a risk.

Every investment has a different risk profile. Cash isn’t

volatile but it is poor at beating inflation. Equities beat

inflation in the long run but aremore volatile in the

short run. Understanding your own risk profile is critical

as it is the only way to build a portfolio that will meet

your long term goals – you need to know:

EGGS, BASKETS

&OMELETTES

AS A RULE OF THUMBMORE OFTEN

THAN ANNUALLY AND LESS OFTEN

THANQUARTERLY IS AGOODGUIDE

– THE COSTS OF REBALANCING

BEING A KEY FACTOR.

“WOULDYOU TELLME, PLEASE,WHICHWAY I OUGHT TOGO FROMHERE?”

“THATDEPENDS AGOODDEALONWHERE YOUWANT TOGET TO”,

SAID THE CAT.

Spending some time to develop this plan is probably

themost important stage in investing.

Without a plan howwill you knowwhether you are on

track? This is an area where a good financial adviser

can really help. And any plan will of course need to

understand the risks.

•

Your attitude to risk (your appetite for risk if you like)

•

Your need for risk (howmuch return do you need to

meet your goals?)

•

Your risk tolerance (can you afford short term losses

in pursuit of longer term goals?)

Many investors underestimate the impact of inflation or

as Neil Rossiter (Certified Financial Planner) describes it

‘the hidden tax’.

Many people aged 60 today will live into their 80s and

beyond. To keep pace with inflation at just 2.5% pa your

investments need to grow by 85% over a 25 year period.

Your investment plan needs to take account of this.